The Rubber Economist Ltd

Natural rubber shortage

What becomes clear to us when examining longer term projections of natural rubber (NR), is the likelihood of a shortage in the future. One does not even need a forecasting model to foresee coming shortages in NR. In recent years, steady economic development in NR producing countries has and will influence the sustainability of NR. While other commodities may be in structural surplus because demand may be declining on a per capita basis, and hence prices may be expected to continue to fall further, there is one factor which may cause NR shortages and prices to increase in the longer term. NR is unique because two of the three major producing countries, Thailand and Malaysia – possibly to be followed by Indonesia – are among the world’s fastest growing economies and are likely to be the next generation of Newly Industrialized Countries (NICs).

On the demand side, the saturation effects on rubber consumption in developed countries are still expected, but it is likely that consumption will pick up elsewhere, particularly in the Asia/Pacific region, and this will be more than enough to compensate for any decline in demand in the developed countries. There will be plenty of room for increasing rubber consumption in the Asia/Pacific region, considering its current low rubber consumption per capita in relation to that achieved in the developed world. In addition, this region has the world’s highest economic growth rate. The final effect is that there will continue to be growth in world elastomer consumption and the centre of gravity will continue to shift from North America and Europe to Asia/Pacific.

On the supply side, the most important factor determining availability of rubber is the cost of producing rubber: not the accounting cost of inputs such as fertilisers, but the ‘opportunity’ cost of producing rubber. The decision to plant or to tap rubber trees depends not only on current prices, but also on alternative incomes and alternative costs. The land, capital and labour that go into producing rubber means that, for example, opportunities for building a factory or industrial complex for example are lost. In the early stage of economic development in a rubber producing country the opportunity cost of rubber production is quite low. There were few opportunities in Malaysia, for example, apart from producing rubber and other commodities 20–30 years ago and wages in the city were not high enough to attract tappers away from the plantations. As a result, Malaysian rubber output increased rapidly. During the last 20 years the opportunity cost has increased. As the country industrialised, higher wages in the city attracted workers and made land and capital relatively expensive to produce rubber. This explains why Malaysian rubber output has declined from its peak and now ranks as only the seventh largest producing country.

The increasing opportunity cost will eventually be faced by all rubber producing countries when the time comes. Next will most likely be Thailand, followed by Indonesia. History, the top three NR producing countries were Malaysia, Indonesia and Thailand. Malaysia have been increasing their emphasis on the manufacturing sector at the expense of the agricultural sector. Most Malaysian plantation workers are now foreigners, whose employment requires a government levy plus recruitment expenses. However, after a few months many move to find jobs in the higher-paid manufacturing sector. Malaysia, Thailand and Indonesia have developed downstream commodity industries, e.g. Malaysia is now the world’s largest producer of latex rubber-goods.

As demand continues to increase while supply declines, the NR industry will eventually face shortages. NR is an export commodity and as the major NR producing countries use more, less is available for export. NR production will become more and more capital intensive and yields will continue to increase while acreage declines and globalisation will be an important factor influencing rubber demand. Prices will continue to be subject to short-term fluctuations, by weather, currency movement, futures market activities, irregular demand and so on. In the medium–term, prices will also continue to move in a cyclical manner, influenced by economic growth. In the long-term, when shortages arrive, there will be pressure on prices. The NR price is likely to perform better relative to prices of other commodities, which will decline relative to the prices of manufactured products. There may be an increase in the use of SR as a petroleum based product, which is not beneficial ecologically.

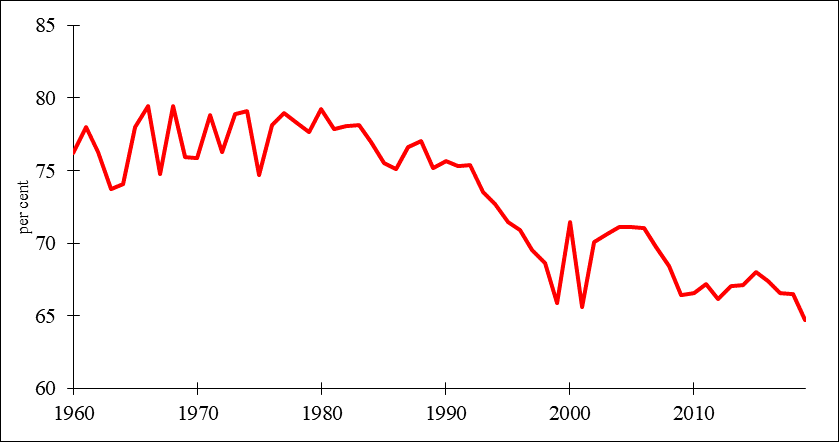

There are prospects for improvements in supply from smaller NR producing countries. Some of these countries are embarking on expansion plans and programmes to boost production and privatization programmes are underway to attract further investment. The prospects for expansion have been helped in recent years by relatively high prices. African rubber was also helped by the Common Fund for Commodities (CFC), which sponsored a project which aimed to improve the quality of rubber produced in West Africa by producing Technically Specified Rubber under a common Professional Association of Natural Rubber in Africa (ANRA) label. The Common Fund also sponsored the IRSG International Rubber Forum in Cameroon in March 2004, allowing certain individuals from key producing countries to attend the Forum in Limbe. However, it is increasingly difficult to see output in small producing countries as enough to make an appreciable difference in the international markets. As can be seen in the graph below that the share of Malaysia, Indonesia and Thailand has only slowly been declining and output, from two of the most rapidly growing areas, i.e., China and India, is mainly geared toward domestic consumption.

The share NR output from Thailand, Indonesia and Malaysia, 1960–2019

Copyright © 2020 - The Rubber Economist Ltd, All rights reserved.

Please contact [email protected] for more information.